Meter

Quarterly Results Intelligence

KSB Ltd

Management Guidance

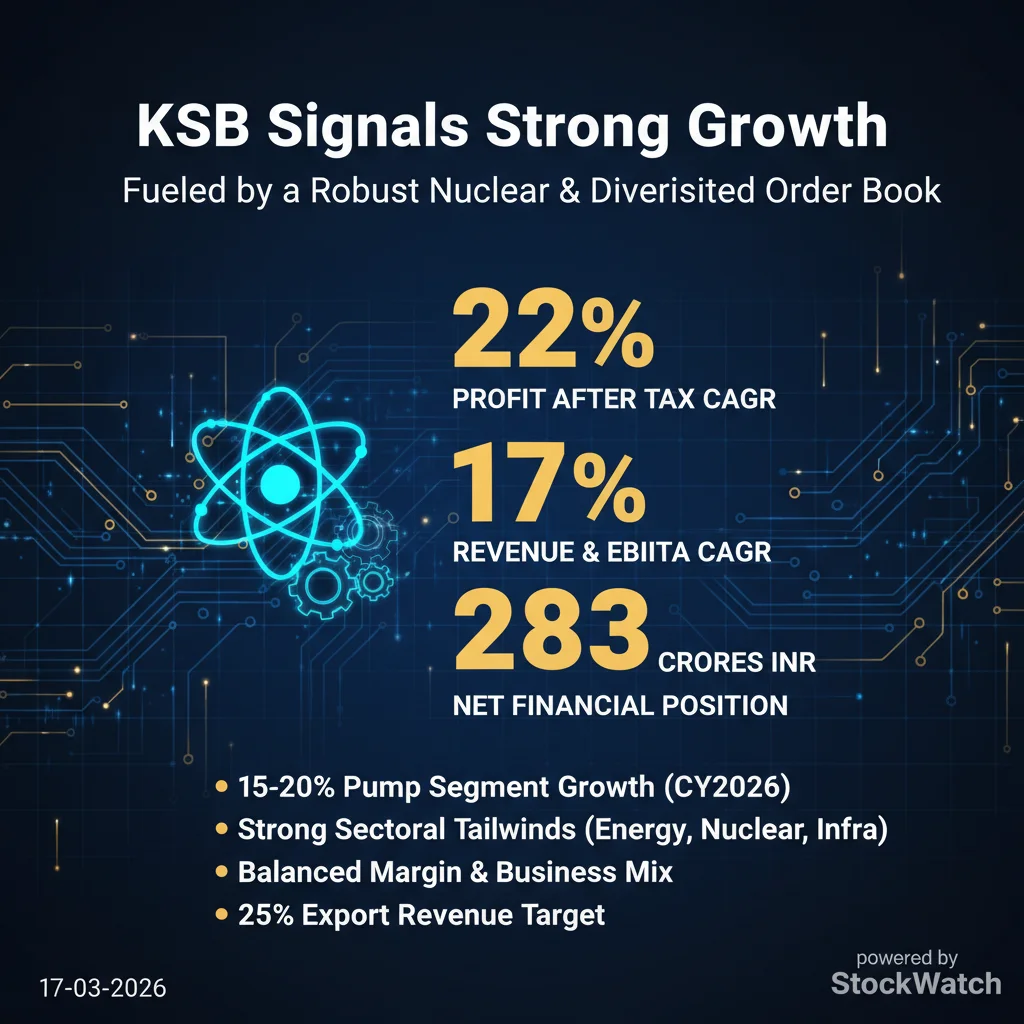

Management guides for 15-20% revenue growth in the pump segment for CY2026, driven by a strong order book and the commencement of nuclear project execution. The company aims to maintain EBITDA margins around 13-14% by balancing project business with high-margin aftermarket and export sales, though commodity price volatility is a key watchpoint. Strategic focus remains on capitalizing on the decadal nuclear opportunity, expanding in solar and water infrastructure, and growing the profitable SupremeServ aftermarket business.

P/L Statement (in cr.)

Press Releases

Earnings Call Recordings

Positive Outlook

KSB Signals Strong Growth Fueled by a Robust Nuclear & Diversified Order Book

KSB Ltd · KSB

Management Guidance

Management guides for 15-20% revenue growth in the pump segment for CY2026, driven by a strong order book and the commencement of nuclear project execution. The company aims to maintain EBITDA margins around 13-14% by balancing project business with high-margin aftermarket and export sales, though commodity price volatility is a key watchpoint. Strategic focus remains on capitalizing on the decadal nuclear opportunity, expanding in solar and water infrastructure, and growing the profitable SupremeServ aftermarket business.

Omnitech's Growth Surge: Massive Order Book & Margin Expansion Fuel Very Optimistic Outlook

Omnitech Engineering Ltd · OMNI

Management Guidance

Management projects a continuation of its historical revenue CAGR of 35-40%, underpinned by a robust INR 2,900 crore order book with a 3-5 year execution timeline. The company expects to maintain strong EBITDA margins in the 33-38% range, driven by its high-value, precision-engineered product mix. Strategically, the focus is on disciplined execution, leveraging newly added capacity, commencing work on the new Chhapra facility, and expanding into high-growth sectors like gas turbines, defense, and aerospace.

PNGS Reva's Maiden Call: Strong Q3 Results Fuel Aggressive IPO-Funded COCO Expansion Plan

PNGS Reva Diamond Jewellery Ltd · PNGSREVA

Management Guidance

Management outlined an aggressive expansion plan to open 15 new COCO (Company-Owned Company-Operated) stores over the next 24 months, funded by IPO proceeds of approximately INR 287 crores for capex and INR 35 crores for marketing. While this expansion is expected to cause a near-term margin dilution of 100-300 basis points due to marketing spend, the company is confident in growing absolute profitability. New stores are projected to achieve breakeven within 12-24 months, driving the company's long-term growth by shifting from a regional SIS-based model to a pan-India standalone brand.

Markolines Projects 40-50% Growth Fueled by Strong Order Book, Eyes ₹1000 Cr Revenue Target

Markolines Pavement Technologies Ltd · MARKOLINES

Management Guidance

Management guides for 40% to 50% revenue growth in the upcoming fiscal year, driven by a robust unexecuted order book of Rs. 695 crores. While margins are expected to remain steady with profitability driven by volume, the company is strategically targeting a Rs. 1000 crore revenue milestone within three to four years. This long-term growth will be pursued by leveraging enhanced credentials to bid directly for larger NHAI projects, which is expected to improve visibility and performance.

Aye Finance Signals Strong Growth & Profitability Rebound, Targeting 30% CAGR and 4.5% ROA

AYE

Management Guidance

Management is on track to achieve 29-30% AUM growth for FY26 and is targeting a consistent 30% CAGR over the next three years. They expect credit costs to continue declining, targeting a normalized long-term range of 3.25-3.75%. This improvement, combined with operating leverage from recent investments, is expected to drive ROA to between 4.0% and 4.5%, supported by a strategic AUM mix of 30% mortgage and 70% hypothecation loans.

Blue Cloud Unveils Ambitious AI Data Center Strategy with Aggressive Long-Term Revenue Guidance

Blue Cloud Softech Solutions Ltd · BLUECLOUDS

Management Guidance

Management provides very strong long-term guidance, projecting approximately Rs. 3,000 crores in revenue for FY 2027, followed by 25-30% year-on-year growth. This growth is heavily reliant on a new, capital-intensive AI data center business, which is planned to roll out starting in FY 2028 with a total Phase 1 CAPEX of $350 million. The data center is projected to scale to 100 megawatts by FY 2032, with target EBITDA margins expanding from 16% to nearly 50% as occupancy rates increase.

PCL Locks in Long-Term Growth with INR 1,500 Cr Order Book, Pivoting EV Strategy Amid Market Shifts

Precision Camshafts Ltd · PRECAM

Management Guidance

Management provided a strong outlook, underpinned by new orders worth approximately INR 1,500 crores that extend the order book to 2032 and enhance long-term revenue visibility. The company is investing INR 120 crores in capacity expansion to support these new programs, which are scheduled to ramp up starting in FY26-27. Strategically, the focus is on the resilient Indian ICE market, leveraging the global EV slowdown, while pivoting its domestic EV efforts towards the heavy commercial vehicle segment and actively seeking acquisitions in adjacent manufacturing sectors in India.

RACL Geartech: Strong Growth & Margin Expansion Driven by Strategic Capex and New EV/EPS Wins

RACL Geartech Ltd · RACLGEAR

Management Guidance

Management has issued a revenue guidance of ₹565 crores (+/- 5%) for FY27, representing approximately 17% growth, supported by a planned CAPEX of ₹77.45 crores. This investment is strategically allocated towards a major heat treatment plant upgrade for backward integration and cost efficiency, alongside capacity expansion for new projects. Growth is expected to be driven by the ramp-up of the BMW electric car business, a new ZF electric power steering project for trucks, increased volumes from a premium two-wheeler client, and the ongoing stabilization of the KTM business.

Schaeffler India Q4 CY25: Strong Growth Across Segments, Bullish on 2026 with Increased Capex & EV Focus

Schaeffler India Ltd · SCHAEFFLER

Management Guidance

Management projects sustained double-digit growth into 2026, driven by a strong pipeline of business wins across automotive (ICE, hybrid, and EV), industrial, and aftermarket segments. The company plans to increase capex to over INR 500 crores in 2026 to support capacity expansion and localization initiatives. While the exceptional export growth seen in 2025 is expected to moderate to a 5-10% range, the overall domestic demand outlook remains very strong, supported by positive macroeconomic indicators and sector-specific reforms.

Triton Valves: Firing on EV & TPMS Growth, Aiming for Higher Margins Amid Climate Control Hurdles

TRITON VALVES LTD. · TRITONV

Management Guidance

Management projects group sales to exceed 550 crores for the current year, targeting a long-term CAGR of 20-25%. They are focused on driving EBITDA margins above 10% in the coming quarters through price corrections and a richer product mix, particularly from high-growth TPMS and EV segments. While the climate control vertical faces significant headwinds from Chinese dumping, the company is actively pursuing government intervention to unlock its substantial market potential and will continue prudent CapEx of 5-8 crores annually in the automotive vertical to support growth.

Cautious Outlook

Fractal Reports Strong Q3 Growth and Margins, Outlines Ambitious Long-Term AI Strategy

FRACTAL

Management Guidance

Management did not provide specific quantitative guidance but expressed a long-term aspiration to return to its historical ~30% CAGR, driven by the enterprise AI expansion. They expect to expand best-in-class gross margins through a shift to output-based contracts and productivity gains. While R&D investments will remain significant, management anticipates adjusted EBITDA and PAT margin expansion over time, driven by operating leverage in SG&A and lower relative ESOP costs.

Avanti Feeds: Tariff Relief Boosts Outlook Amidst Rising Raw Material Costs

AVANTI FEEDS LTD.-$ · AVANTI

Management Guidance

Management guides for FY26 feed sales of approximately 555,000 MT and shrimp exports of 16,500 MT, with an expected minimum 10% feed volume growth in the upcoming year driven by a strong start to the culture season. However, they caution that steep increases in raw material prices will impact Q4 margins, bringing the full-year FY26 feed PBT margin to an estimated 14.5-15%. The long-term strategy focuses on scaling the processing business, benefiting from improved US market access and potential EU/UK trade deals, and establishing the new pet food business with a manufacturing facility under development.

Dhruv Consultancy Grapples with Major Accounting Revision Amidst Strong Order Book and Diversification Push

Dhruv Consultancy Services Ltd · DHRUV

Management Guidance

Management provided no quantitative guidance for Q4 but stated the current unexecuted order book of INR 256 crores offers revenue visibility for the next 2.5-3 years. They emphasized that the INR 30 crore accounting adjustment was a one-time, non-cash event due to a shift to a more conservative estimation method and assured it would not be repeated. Strategically, the company is focused on executing its strong order book, diversifying into new sectors like airports and geographies like the Middle East to de-risk its profile and improve future margins.

Dhruv Consultancy Grapples with Major Accounting Revision Amidst Strong Order Book and Diversification Push

Dhruv Consultancy Services Ltd · DHRUV

Management Guidance

Management provided no quantitative guidance for Q4 but stated the current unexecuted order book of INR 256 crores offers revenue visibility for the next 2.5-3 years. They emphasized that the INR 30 crore accounting adjustment was a one-time, non-cash event due to a shift to a more conservative estimation method and assured it would not be repeated. Strategically, the company is focused on executing its strong order book, diversifying into new sectors like airports and geographies like the Middle East to de-risk its profile and improve future margins.

Sanofi India's Transformation: Core Diabetes Growth Buffers Partnership Volatility

Sanofi India Ltd · SANOFI

Management Guidance

Management expects continued strong growth from its core diabetes franchise, driven by Soliqua and Toujeo and expansion into the public sector. However, they explicitly guided for continued sales volatility and fluctuations in the partnered portfolio through 2026, with stabilization anticipated by year-end. The company will focus on operational efficiencies to maintain profitability and has no new product launches planned for 2026, relying on its current portfolio and partnership model to drive future performance.

Ola Electric's Reset: Fixing Service & Slashing Costs While Touting Margin & Gigafactory Strength

Ola Electric Mobility Ltd · OLAELEC

Management Guidance

Management guides for gross margins to stabilize between 35-40% in FY27, driven by deep vertical integration. A major cost reset is underway, targeting a steady-state quarterly OpEx of ₹250-₹300 crores, which lowers the EBITDA breakeven point to approximately 15,000 units per month. With the heavy capex cycle now complete, the strategic focus is on fixing service execution to rebuild brand trust and drive sales recovery, while scaling the Gigafactory to 6 GWh by March 2026.

Exato Q3: Strong Growth & Profitability, Eyes Aggressive Global Expansion and AI-Powered IP

Exato Technologies Ltd · EXATO

Management Guidance

Management guided for a strong finish to FY26 with 25-30% revenue growth and 50-60% PAT growth, despite potential quarterly fluctuations due to large deal cycles. The core strategic focus is on aggressive international expansion into the US, Australia, and UK to capture higher margins and diversify revenue. This global push will be supported by the expedited commercial launch of proprietary IP platforms, with revenue expected from Q3 FY27, and an openness to strategic M&A to accelerate growth.

Exato Q3: Strong Growth & Profitability, Eyes Aggressive Global Expansion and AI-Powered IP

Exato Technologies Ltd · EXATO

Management Guidance

Management guided for a strong finish to FY26 with 25-30% revenue growth and 50-60% PAT growth, despite potential quarterly fluctuations due to large deal cycles. The core strategic focus is on aggressive international expansion into the US, Australia, and UK to capture higher margins and diversify revenue. This global push will be supported by the expedited commercial launch of proprietary IP platforms, with revenue expected from Q3 FY27, and an openness to strategic M&A to accelerate growth.

Maan Aluminium: Navigating Capex Ramp-Up & Muted Demand, Targeting High-Value Segments

MAAN ALUMINIUM LTD. · MAANALU

Management Guidance

Management is guiding for a gradual ramp-up, targeting over 18,000 tons of volume and INR 500 crores in manufacturing revenue in the next fiscal year. The strategic focus is on transitioning to high-value products for aerospace and defense to achieve normalized EBITDA margins of around 8% and a consolidated EBITDA of USD 450 per ton in the medium term. This will be driven by a ~INR 190 crore capex plan to expand value-added capabilities like anodizing, powder coating, and precision tubing at the new Dewas facility, which is expected to commission within 6-8 months.

Godavari Bio: Strong Profit Growth Driven by Bio-Chemicals Amidst Near-Term Ethanol Headwinds

Godavari Biorefineries Ltd · GODAVARIB

Management Guidance

Management reiterates its strategic goal of achieving 3x EBITDA by FY29 (from an FY25 baseline), supported by a planned capex of INR 325 crores, with 75% allocated to high-margin bio-based chemicals. The delayed grain-based distillery is now expected to be commissioned in the next quarter, enhancing feedstock flexibility. While no specific quantitative guidance was provided, the company is focused on scaling its specialty chemicals portfolio, advancing innovation projects like DME and cancer molecules, and capitalizing on the long-term green transition trend.